The Unclaimed Asset Recovery Process Explained: What Consumers Should Know Before Filing a Claim

You may know that billions of American dollars in forgotten funds sit in government vaults. However, you might not know how to recover these unclaimed assets. The gap between knowing an asset exists and successfully cashing a check is where most people get stuck.

As per NAUPA’s report, state programs returned a record $4.49 billion to owners during the 2024 fiscal year. While you may think that number is high, it is a small fraction of the roughly $70 billion that remains unclaimed, as per the letter of Meaghan Aguirre, Director of Unclaimed Property at the State of Nebraska. The reason for this backlog is a lack of public awareness as well as administrative friction in the recovery framework itself.

Filing a claim is a formal legal procedure. It requires specific evidence that many people no longer have, such as proof of an address from thirty years ago. This article explains the technical steps of the recovery process to set accurate expectations for consumers. Find out more below:

How Unclaimed Assets End Up With State Agencies?

The legal process of claiming or abandoning property to a state treasury is called escheatment. This legal rule stops companies from keeping dormant funds as profit. Instead, banks, insurance companies, and former employers must send these assets to the state after a set period of no contact. This timeframe is the dormancy period.

Most dormancy periods last between one and five years. Before a company sends the money to the state, it must try to find the owner. This is known as “due diligence,” and it usually involves mailing a notice to the last known address on file.

If that letter goes unanswered, the funds are reported and remitted during the state’s annual reporting cycle. Many states require these reports by either October 31 or November 1.

With that said, the following table sums up the typical dormancy period for different asset types:

| Asset Type | Examples | Typical Dormancy |

| Liquid Accounts | Savings, checking, or CDs | 3 to 5 years |

| Payroll | Uncashed wages or commissions | 1 year |

| Insurance | Life benefits or premium refunds | 3 to 5 years |

| Refunds | Utility or security deposits | 1 to 3 years |

| Valuables | Jewelry or coins from safe deposit boxes | 5 years of unpaid rent |

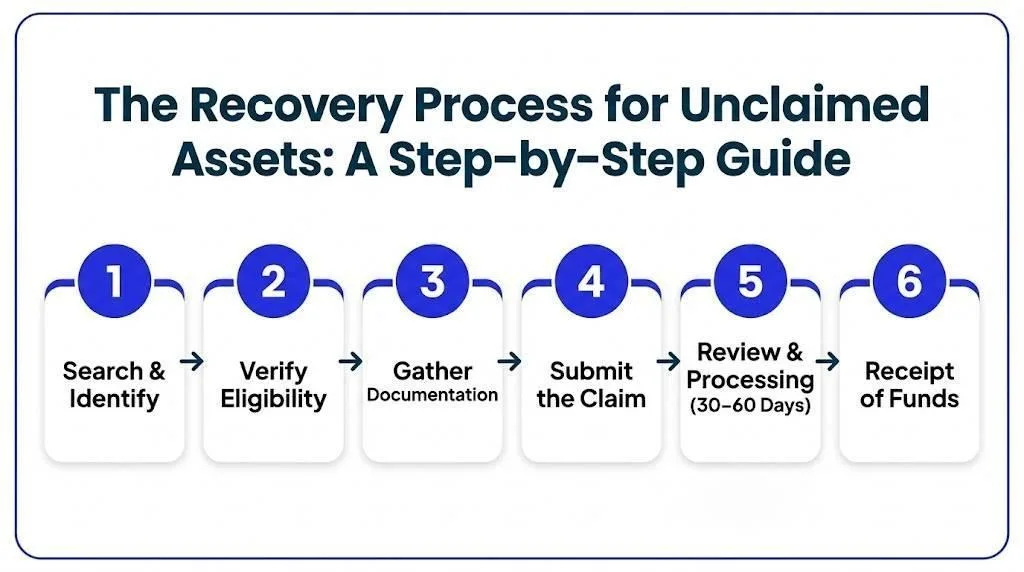

The Recovery Process for Unclaimed Assets: A Step-by-Step Guide

The recovery path for the unclaimed assets involves multiple steps. However, as simple as it seems, this process can be complicated due to multiple reasons. Let’s consult the following section to understand the step-by-step recovery process for the unclaimed assets:

Step 1: Search and Identify

The first step starts with a basic search. Because people move across state lines, your money might be in a treasury far from where you live now. Most states use MissingMoney.com, which is a national database managed by NAUPA.

Step: Verify Eligibility

Finding a name match is not enough. You have to prove the specific record belongs to you. You can do this by looking at the “holder” information, which is the name of the company that reported the money. If you have never had an account with that bank or utility provider, the money likely belongs to someone else with the same name. Some quick things that you can do are mentioned in this table:

| Factor | What to Check | Why it Matters |

| Original Holder | The bank or employer | Confirms you had a relationship with them. |

| Last Address | The address on the record | Links your identity to that specific file. |

| Property Type | Source (e.g., insurance refund) | Matches your financial history. |

Step 3: Gather Documentation

This is the hardest part for most people and probably the biggest reason why people give up on this process. Every state needs a copy of your ID and proof of your Social Security number. However, you also need to prove you once lived at the address listed on the record.

If the account is old, you might need to find tax forms, school transcripts, or old utility bills. On top of that, if the owner is deceased, you will need a death certificate and proof that you are the legal heir. This often includes a will, probate documents, or a table of heirship.

Step 4: Submit the Claim

Most states allow you to upload your files through an online portal. You can even submit the claim via the official government-approved digital tools. If the claim is for a high dollar amount or involves a safe deposit box, you may still have to mail in a physical form that has been signed in front of a notary.

Some states are trying to simplify the claiming process. For example, Pennsylvania, Illinois, and Oregon have Money Match programs. These initiatives automatically send checks to people for low-value and single-owner claims without requiring any paperwork. Pennsylvania’s program returned more than $50 million in its first year (2025), as per the Pennsylvania Treasurer.

Step 5: Review and Processing

After you submit, an auditor reviews your files. This step takes time, often around 30 to 60 days. In fact, it can take months for complex cases, like those for an estate. If the state needs more info, they will send a letter. That request usually resets the processing clock, so it is best to be thorough on the first try.

Step 6: Receipt of Funds

If your claim is valid and approved, the state sends the payment. This is usually a check in the mail, but some states also send the direct deposit to your accounts. For the claim of physical items like jewelry, the state might arrange a secure delivery.

If the items were already sold at a state auction, you will get the cash proceeds from that sale. States hold these auctions periodically to make room for new property, but the cash remains available for you to claim indefinitely.

Common Complications During the Unclaimed Assets Recovery Process

The recovery process of unclaimed assets is not very simple. Particularly, the paper submission step as well as the attendance on-call letter are quite tough steps. Apart from that, there are some complications that often lead the process to hit a wall. A list of these complications is given below for your awareness:

- Name Changes: If your name on the record (like a maiden name) doesn’t match your ID, you need a bridge document. This could be a marriage license or a court order for a name change.

- Inherited Claims and Probate Limits: States must be sure you are the right heir. Every state has a “small estate” limit. If the money is worth more than that limit, you have to go through a full probate court process, requiring the services of a probate lawyer.

- Corporate Errors: Sometimes the company that reported the money made a mistake. For example, they might have reported a check but left the owner’s name as unknown. In these cases, you might have to get a letter of verification from the original company, which is quite hard.

- Out-of-State Records: Companies often send money to the state where they are incorporated, not where you live. For example, your company with unclaimed money is in Delaware and you might live in California. In that case, you have to file a claim with the Delaware treasury.

When does Claim Assistance for the Recovery Process Make Sense?

As explained, the recovery process is not very simple, especially for large transactions or unknown owners. Likewise, documenting everything or recovering funds across states can be a headache for many people. In that case, a third-party claim assistance can be quite helpful.

GovRecover is a company that provides licensed and guided assistance for the unclaimed asset recovery process. The best thing is that this company is state-licensed, which involves background checks and fingerprinting of its principals in applicable states. Plus, GovRecover operates on a contingency basis, meaning there are no upfront fees. Consumers with questions about the process or about a specific claim can reach the GovRecover support team at (844) 931-3123.

Conclusion

The TL;DR is that the unclaimed asset recovery process is easy to manage if you try to handle things carefully. To make things easy, always keep a record of checks and update your addresses with banks or employers. Plus, you should also check the state database on a yearly basis to learn about your financial health. With that said, if you are stuck in the asset recovery process, GovRecover’s support team can be quite useful for you. You can reach them via (844) 931-3123 or through GovRecover.org.

Frequently Asked Questions

How long does an unclaimed asset claim typically take?

An unclaimed asset claim can take 2 to 3 months. However, it is process and state-dependent. If you have a simple or short claim, the state will pay you in just a few weeks. For complex cases or higher amounts, you might have to wait for months.

What documents do I need to file an unclaimed asset claim?

You need a signed claim form, photo ID, and your SSN to file an unclaimed asset claim. Apart from these basic requirements, the officers may ask you to submit other records like bank statements, addresses, rental agreements, bills, or tax records.

Can I claim assets on behalf of a deceased relative?

Yes, you can claim assets on behalf of a deceased relative. It would be easier if you were a legal heir, appointed executor or administrator. However, you might have to submit documents to show that you are eligible to recover the funds.

What happens if my claim is incomplete?

If your claim is incomplete, you won’t be able to recover the funds. The treasurer will ask for more proof. Further, this will lead to restarting the entire process. Therefore, you should always submit all the required documents to avoid any issues.

How can GovRecover help with a claim?

GovRecover helps you with a claim by finding the assets and then verifying your eligibility. Plus, they can also prepare the documents on your behalf. You can access their support team at (844) 931-3123.