How Technology Is Transforming Accounting And Why CPAs Are More Crucial Than Ever

Examining the intersection of innovation, automation, and expert financial guidance in the modern business world

Since the invention of double-entry bookkeeping in tucson, the accounting profession has undergone its most significant transformation. In 2026, technology serves as the primary infrastructure for all modern financial operations. Recent surveys show that 88% of finance executives believe artificial intelligence (AI) will be the most transformative trend in accounting over the next two years.

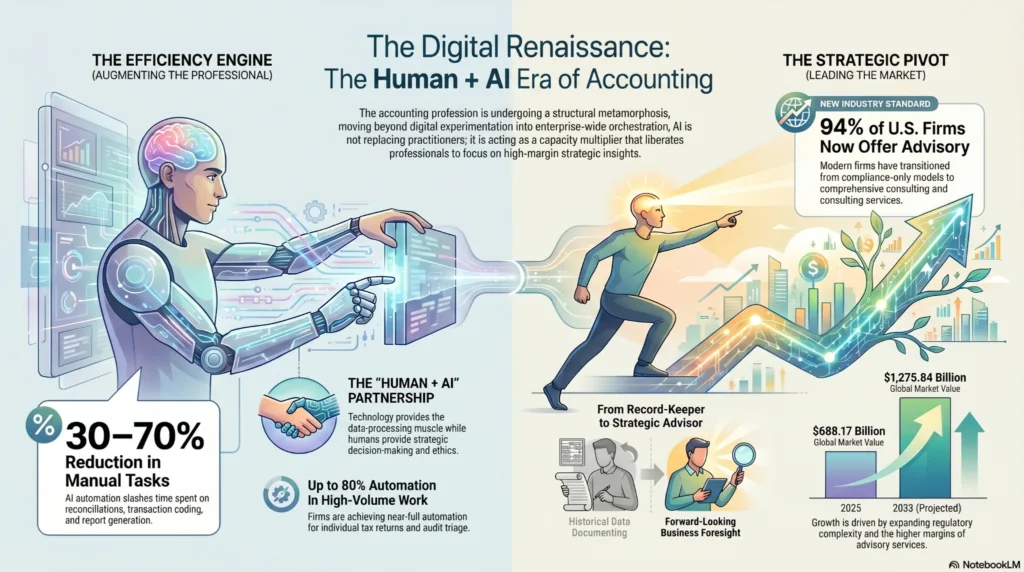

While automation, AI, and cloud computing are rapidly changing financial workflows, this adaptation is not replacing professionals; it is enhancing their potential. The current environment is defined by a “Human + AI” partnership, where machines handle processing and data tasks, while CPAs provide judgment, strategy, and ethical oversight. Even with these technological advancements, Certified Public Accountants (CPAs) are still important for guiding and making decisions in a complex financial world.

Evolution of Accounting Technology

Accounting has moved rapidly from manual ledgers to intelligent, AI-supported systems. Traditionally, separate ledgers required time-consuming reconciliations and were prone to error. Today, several technologies are driving a profound change:

- Cloud Accounting Platforms: Modern platforms like QuickBooks Online and Xero function as more than digital ledgers. They are now integrated ecosystems where AI agents can work directly on source data. This improves accuracy and reduces processing time.

- Artificial Intelligence & Machine Learning: Apart from calculations, AI and ML are used for fraud detection, audit analysis, and predictive cash flow forecasting, identifying patterns that humans may miss.

- Robotic Process Automation (RPA): RPA performs as a “digital worker,” executing repetitive tasks like data entry and invoice processing at remarkable speed.

- Blockchain: This secure, decentralized ledger creates a single, transparent source of truth. Blockchain can reduce reconciliation efforts by up to 65%, which enables auditors to focus on system assurance rather than manual checks.

This advancement allows accounting firms to move from historical record-keeping to forward-looking advisory services and provide strategic insights rather than just financials.

Benefits of Technology in Accounting

By integrating technology into accounting workflows, it provides measurable improvements, such as:

- Time Savings and Efficiency: Firms that are using AI-powered automation report 30%-70% time savings on tasks like bank reconciliations and transaction coding.

- Enhanced Accuracy: Automation reduces human errors as AI can scan entire data sets, and anomalies can be flagged that traditional sampling would miss.

- Real-Time Insights: Cloud-based tools and AI enable continuous review and live financial reporting, which helps business owners to make immediate, informed decisions.

- Risk Management: Modern systems include built-in compliance checks and audit trails that keep firms aligned with evolving regulations.

For instance, a media production client using a centralized AI-supported system saw a 35% reduction in expenses by improving decentralized, manual processes.

Why CPAs are Still Important

Despite advances in technology, humans are still the final authority on trust. Machines cannot sign financial statements or assume legal and ethical responsibility.

CPAs bring several irreplaceable capabilities:

- More Than Record-Keeping: CPAs now work as strategic advisors, not just record-keepers. AI can model risks, but it cannot set a vision or lead a company toward its mission.

- Critical Thinking & Judgment: AI recognizes patterns, but only CPAs can interpret variances within context, distinguishing a temporary market fluctuation from a fundamental business change.

- Ethics and Compliance: High-stakes financial environments require human oversight to prevent opaque “black box” systems.

- Advisory Roles: Technology can highlight opportunities, but CPAs guide clients through tax planning, leadership transitions, and complex decisions.

As businesses in fast-growing areas like Fayetteville adapt to a digital economy, CPAs play a more vital role than ever, bridging financial expertise and technological execution.

How CPAs Are Adopting Technology

Modern CPAs in boise idaho are leveraging automation rather than resisting it, emerging as “Digital Seniors” who combine deep accounting expertise with workflow design and AI oversight. By automating repetitive tasks, they can focus on high-impact analysis instead of routine data entry, delivering more value to their clients.

With the help of predictive analytics, CPAs can forecast cash flows, identify risks early, and provide guidance that gets results. The major firms are adopting hybrid models, using robotic process automation (RPA) as the “muscle” for legacy systems and AI as the “brain” for strategic decision-making.

Meanwhile, cloud-based tools enhance communication and real-time collaboration, fostering stronger client relationships built on transparency and trust.

The Future of Accounting

Co-intelligence, an intentional partnership between human and machine, is defining what’s ahead. By 2028, it is estimated that 15% of daily accounting decisions will be made autonomously by AI agents. Continuous auditing, enabled by blockchain and AI, will test for discrepancies in real-time, transforming how firms monitor financial health.

Continuous learning is now a strategic asset. The next generation of CPAs is trained to interpret AI outputs and translate them into actionable business strategies, ensuring insights are not just accurate but meaningful. At JTC CPAs, this approach combines technology with human wisdom to deliver deeper insights without losing personal connection.

Data Analysis: Economic and Operational Impact

Key data points below highlight both the economic and operational impact of emerging accounting technologies.

| Focus Area | Key Metric |

| Market Growth | Global accounting services market projected to grow from $688.17B (2025) to $1.27T (2033) |

| Productivity | AI-powered automation yields 30%–70% time savings on common accounting tasks |

| Advisory Shift | 94% of U.S. firms now offer advisory or consulting services |

| Revenue Impact | Firms offering advisory services see up to a 50% increase in monthly revenue per client |

| Workload Reduction | Organizations adopting intelligent automation report a 40% reduction in manual workload |

| Accuracy Gap | AI provides incorrect advice in complex tax scenarios ~50% of the time, highlighting the need for human review |

Key Takeaways

Technology gives more freedom to the accounting profession, not a replacement. AI completes routine work, blockchain protects financial records, and CPAs provide business advice, careful judgment, and financial planning. In the digital age, professional expertise has greater value than ever before. With modern technology and human knowledge together, businesses can face the financial challenges of 2026 and the future with confidence. A CPA can help your business make better decisions in a fast-changing financial world.